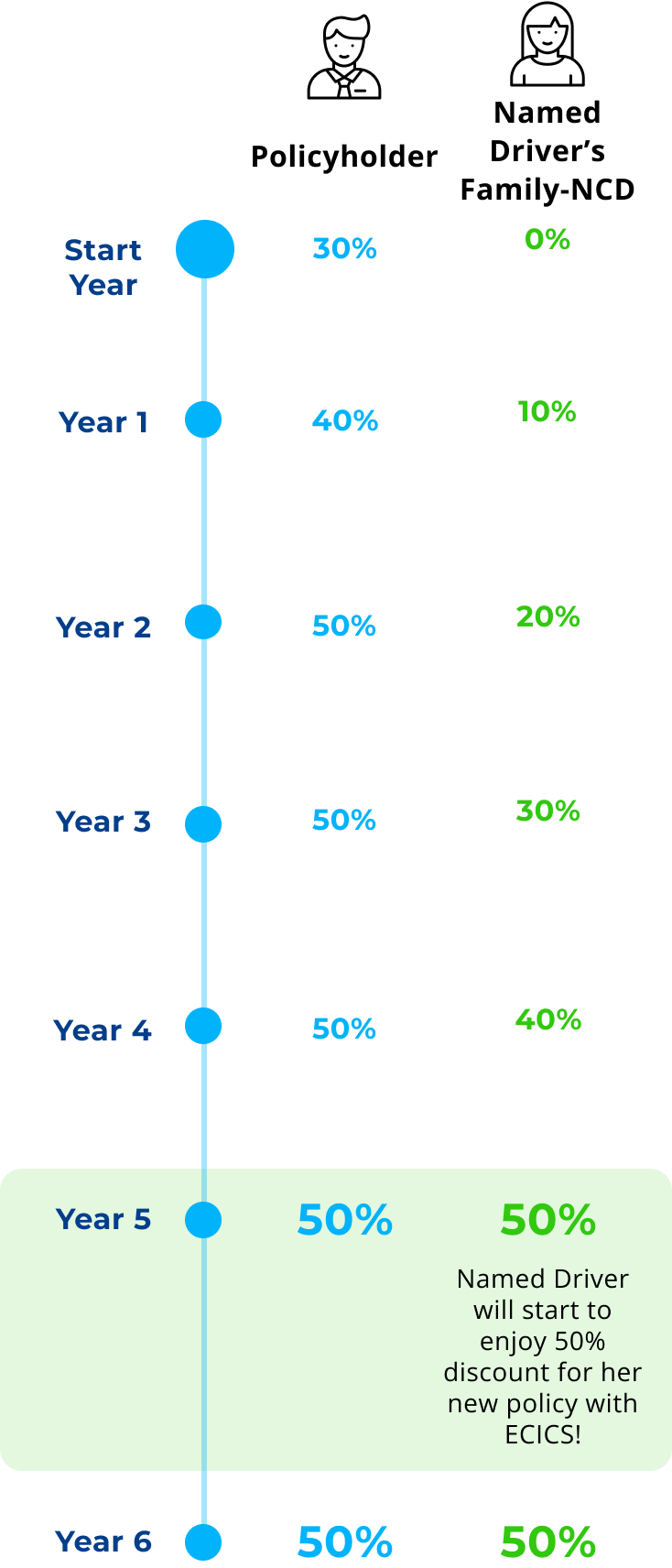

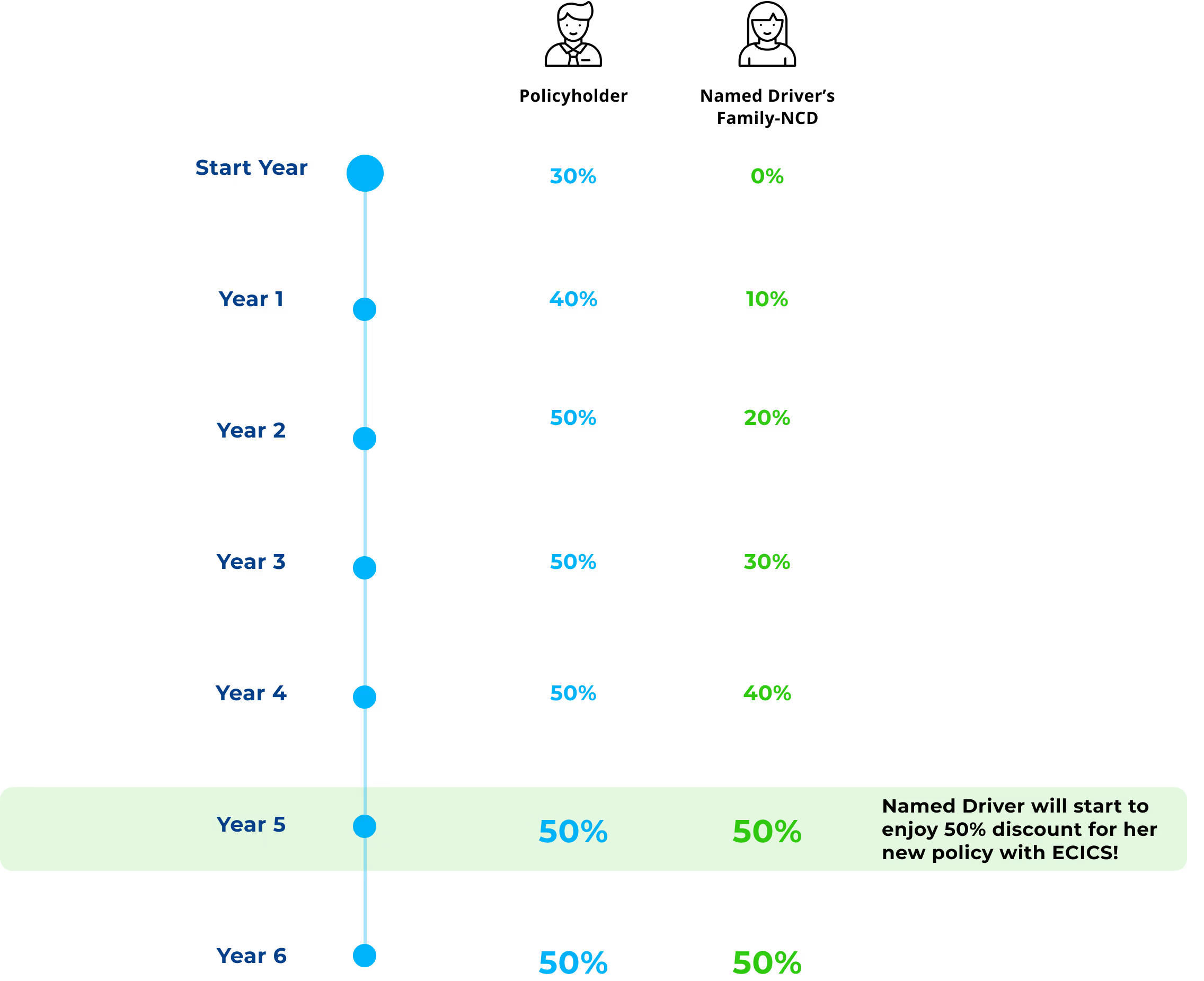

Every named driver earn 10% Family-NCD (up to 50%) for each year of safe driving as a family without any accidents - even if they don't own a car.

When your family member buys their own car, their accumulated Family-NCD can be used to reduce their insurance premium with ECICS.

Includes personal accident coverage up to $80,000 for your family members, child seat protection up to $300, and car key replacement cover up to $300.

Get 24/7 roadside assistance, and up to 10 days courtesy car while your vehicle is being repaired.

Terms and conditions apply. Discount is automatically applied. Not stackable with other promos.

We’re More Than Just an Insurer—We’re Your Neighbour Through Life’s What-Ifs.

A No-Claim Discount (‘NCD’) is an entitlement given to you if no claim has been made under your policy for a year or more with the current/existing insurer. It reduces the premium you have to pay for the following year. This is your insurer's way of recognising and rewarding you for having been a careful driver. There is a standard followed by all insurers in setting the NCD, depending on your type of vehicle (private, commercial or motorcycle) and the period of insurance with no claim. The following table shows how the NCD is set by all insurers across the industry. Private Car Period of insurance with no claim Discount on renewal 1 year 10% 2 years 20% 3 years 30% 4 years 40% 5 years or longer 50% Motorcycle/Commercial Vehicle Period of insurance with no claim Discount on renewal 1 year 10% 2 years 15% 3 years or longer 20%

Most insurers in Singapore will allow you to keep your NCD should there be a break in vehicle ownership for up to 24 months. Some insurers set the timeframe at 12 months. You should contact your insurer for details.

Yes, the following occupations or activities are excluded: - Pilots, aircrew or any occupation involving aviation activities - Full-time military personnel - Police force personnel - Fire fighters - Construction / unskilled workers - Ship crew or workers on board vessels, oil and gas rig workers, offshore workers, stevedores, shipbreakers - Welding - Professional sports teams - Work involving height (exceeding 30 feet above ground or floor level) and/or works underground and/or travel beyond normal speed on land and/or handling of hazardous chemical / electricity - Use of Woodworking tools and machineries - Professional divers and jockeys - Crane Operators

Yes. You must notify us if there are any change in circumstances during the period of insurance affecting the risk such as changes in occupation or country of residence.

Yes, if you change your mind after the policy is issued, please write to us within 14 days from the date of receipt of the policy. We will refund you in full subject to no claims made under the policy.

Yes, the policy will need to be cancelled, and a replacement policy issued.

To implement for MI policies, renewals or extensions with start date effective from:1 July 2023 (Stage 1)• Introduction of a co-payment element* for employers and insurers for amounts above $15,000, up to an annual claim limit of at least $60,0001 July 2025 (Stage 2)• Standardisation of allowable exclusion clauses• Introduction of age-differentiated premiums for those aged 50 and below, and those aged above 50• Requirement for insurers to reimburse hospitals directly upon the admissibility of the claimPlease visit MOM's website here for more information on the MI enhancements.

No, you do not need to pay $5,000 upfront to MOM as we act as a guarantor by issuing a Letter of Guarantee to MOM on your behalf. However, if you or your FDW breaches any of MOM’s rules or conditions, MOM may forfeit the bond and demand for payment from ECICS. In such cases, we will seek recovery of the amount from you.

No, she is not covered unless she is travelling with you. We recommend purchasing a separate travel insurance for your FDW as the coverage would be more comprehensive for overseas situations where medical and evacuation costs are expected to be much higher.

Here's how you can determine the effective date based on each situation:For New FDW:The policy's effective date should be the date your FDW arrives in Singapore. This ensures that insurance coverage begins when the FDW starts her employment duties upon arrival in the country.For Transferred FDW:The policy's effective date should be the day you wish to apply for the issuance of her work permit at MOM. This ensures that insurance coverage is in place when the FDW's work permit is processed and approved for transfer to your employment.For Renewal FDW:The policy's effective date should be one day after the current work permit's expiry date. This ensures that insurance coverage seamlessly continues without any gaps when renewing the FDW's work permit for continued employment.

We have 3 plans to suit your needs. The Comprehensive plan covers loss or damage to your motorcycle, as well as third party liability for bodily injury and property damage.

Yes, it is illegal to use a vehicle in Singapore without a valid insurance cover. At a minimum, you must have third-party insurance, which covers injury or damage caused to other people and their property.

All riders need to be named in the policy. Unnamed riders are not covered.

Our policy covers you when you ride your motorcycle in West Malaysia, the Republic of Singapore and that part of Thailand within 80.5km of the border between Thailand and West Malaysia.

We do not cover usage for food, parcel or other delivery services.

It is not transferrable to other insurers. This is a unique and innovative feature of our product to provide customers and their loved ones the best value they can get.

If there is a claim made under the policy, your NCD will be reduced as follows. Private Car Current NCD NCD after 1 Claim 50% 20% 40% 10% 30% and under 0% Motorcycle/Commercial Vehicle Current NCD NCD after 1 Claim 20%/15%/10% 0%

Excess, also known as the deductible, is the first amount of the claim that the policyholder needs to bear in view of the claim.

.png)